Christmas expenses keep increasing year by year. Your friends invite you over for dinner, and the family keeps expecting thoughtful gifts from everyone. At present, most Irish families are estimated to spend £800 on the festive season. This amount has quite dramatically doubled over the last couple of years.

Let’s be honest here, presents are only the beginning of your Christmas expenditures. For instance, there are several special dinners to be had, festive decorations to buy, and a new outfit for the party. Travel chaos and high prices during peak times are next on the list. I bet your heating bill escalates as well when you are expecting visitors.

When Personal Loans Make Financial Sense?

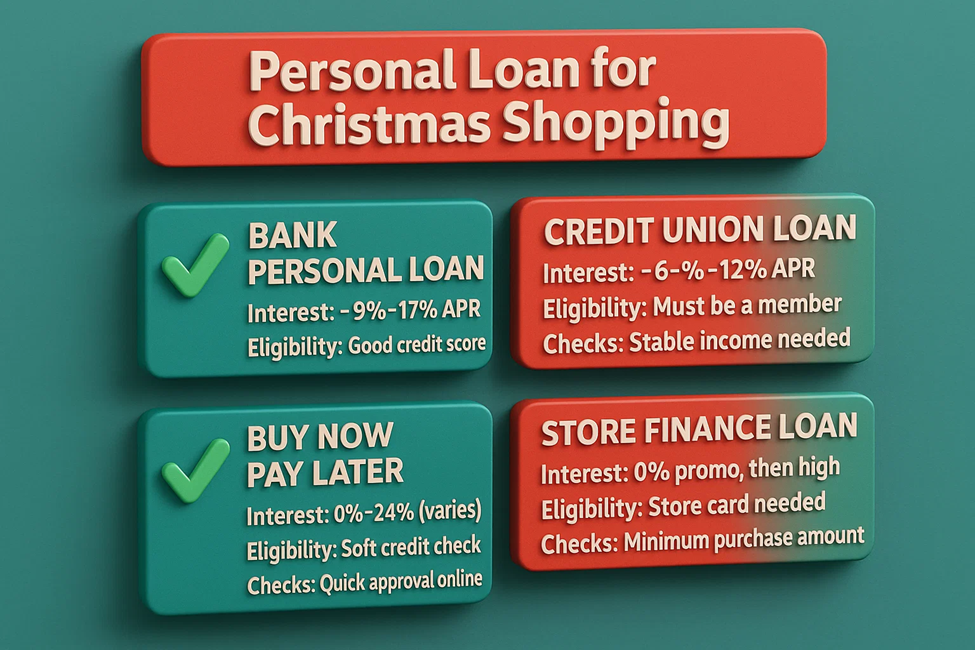

You won’t be spending the same amount of money on all types of borrowing if you decide to borrow for the holidays. If the balance is not paid in full, the credit cards you have will charge interest at 20% or higher. When the promotional rates expire and the regular ones arrive, store cards that seem friendly at first change their rates to 30%.

Compared to other options, taking out personal loans for Christmas is the best way to save money. You will be able to keep track of the money you are supposed to pay each month. Assuming you have a decent credit score, you can get rates between 7% and 12%.

Before you sign any loan agreement, you should set spending limits and make a decision. Can you pay off the debt within half a year without unnecessarily stretching yourself? The smartest thing to do is not only to practice sensible borrowing but also to revise your gift expectations.

The Christmas Money Crunch: Why People Consider Loans

Christmas hits the wallet harder than most of us like to admit. I remember checking my bank balance last December and feeling that sinking feeling. Most families spend about £800-£1,000 on the festive season these days. The gifts are just the start, then come the special food, travel costs, and all those little extras nobody plans for.

January’s bills show up right when your bank account is at its lowest point, the heating costs spike during the coldest month, while you’re still paying for December’s fun. Many of us don’t fully recover from the Christmas splurge until March or April. The cycle repeats year after year, making loans seem like an easy answer.

- Christmas costs keep climbing while wages often stay the same

- Kids seem to expect bigger and better gifts each passing year

- Your regular bills couldn’t care less that you’ve spent your money on gifts

Pros of Using a Personal Loan for Christmas Shopping

Taking out a personal loan saves you money in some cases. Credit cards often charge interest rates of 20% or higher if you can’t pay in full. A personal loan with a fixed rate of 7-12% could significantly cut your costs. You’ll know exactly what you’re paying each month, with no nasty surprises.

The structure of a loan forces you to stick to a repayment plan. With credit cards, it’s too easy to make just the minimum payment. Those small payments stretch your debt out for years, costing you far more. A loan has a fixed end date, so you’ll be debt-free by a certain point.

Having cash in hand gives you better buying power during the holiday season. You might score better deals when you can pay up front rather than using credit. Some shops offer discounts for cash payments to avoid card processing fees. This extra buying power might offset some of the loan interest.

- The interest rate is often lower than credit cards if your credit’s decent

- You won’t max out your everyday cards or mess up your credit utilisation

- The loan has a clear end date, unlike the endless cycle of card debt

- You can shop during early sales with cash rather than waiting for payday

Smart Borrowing Tips if You Still Choose a Loan

Shop around properly before signing any loan agreement. The differences between lenders can be shocking for the same amount. I’ve seen rates vary by 10% or more between different banks. Credit unions often beat the big banks for personal loan rates.

Ask direct questions about any charges you don’t understand fully. A good lender will explain everything clearly without getting annoyed.

For those facing unexpected holiday expenses, options like an instant cash loan in 1 hour in Ireland exist for emergencies. These quick loans can help when sudden costs appear or plans change. However, these should be last resorts due to higher interest rates. Most financial advisors suggest starting with your existing resources.

- Choose the shortest loan term that won’t strain your monthly budget

- Check if there are penalties for paying the loan off early

- Make sure the monthly payment fits comfortably within your income

- Consider whether you really need everything on your Christmas list

Smart Borrowing Tips if You Still Want a Loan

If you’ve decided a loan is your best option for Christmas, don’t rush into the first offer. I’ve seen too many people grab the deal their own bank waves in front of them. The differences between lenders can be huge, sometimes five or six per cent. That might not sound like much, but it adds hundreds of pounds to your total cost.

Rise Of Loan Application During Holidays

| Year | Loan Usage at Christmas (%) | Notes |

| 2023 | ~25% (people struggling to afford Christmas) | 25% struggled; 36% used Buy Now Pay Later (BNPL) |

| 2024 | ~28% (people struggling to afford Christmas) | 28% struggled; BNPL usage rose to 38%; longer repayment times noted |

| 2025 (forecast) | ~30%+ using credit or BNPL to cover spending | 25% adults use BNPL; 14% plan to use BNPL specifically for Christmas 2025 |

- Compare the real APR across at least three different types of lenders

- Watch for early repayment penalties that lock you into the full term

- Read the small print about missed payment fees before signing

Conclusion

The biggest surprise usually comes with the arrival of January’s mail. Receiving those documents is a cold shock of reality. That is why many of them spend the first half of the new year tightening their belts to pay for the last month’s expenses. This financial stress can negatively affect your physical and mental health and strain your relationships. So plan wisely and start budgeting today!

James Wince is the lead author and financial expert at MyLoansBoat. With a decade-long journey in the financial market, he has actually amassed comprehensive understanding and hands-on experience, which he gives his informative, useful, and reader-friendly posts. Covering a broad spectrum of financial subjects – from personal loans to business financing, mortgage refinancing to debt consolidation- James has an incredible capability to break down complicated financial lingo into understandable language, permitting readers to make knowledgeable choices. Enthusiastic about financial literacy, James’s objective is to browse our readers through the frequently frustrating seas of finance.