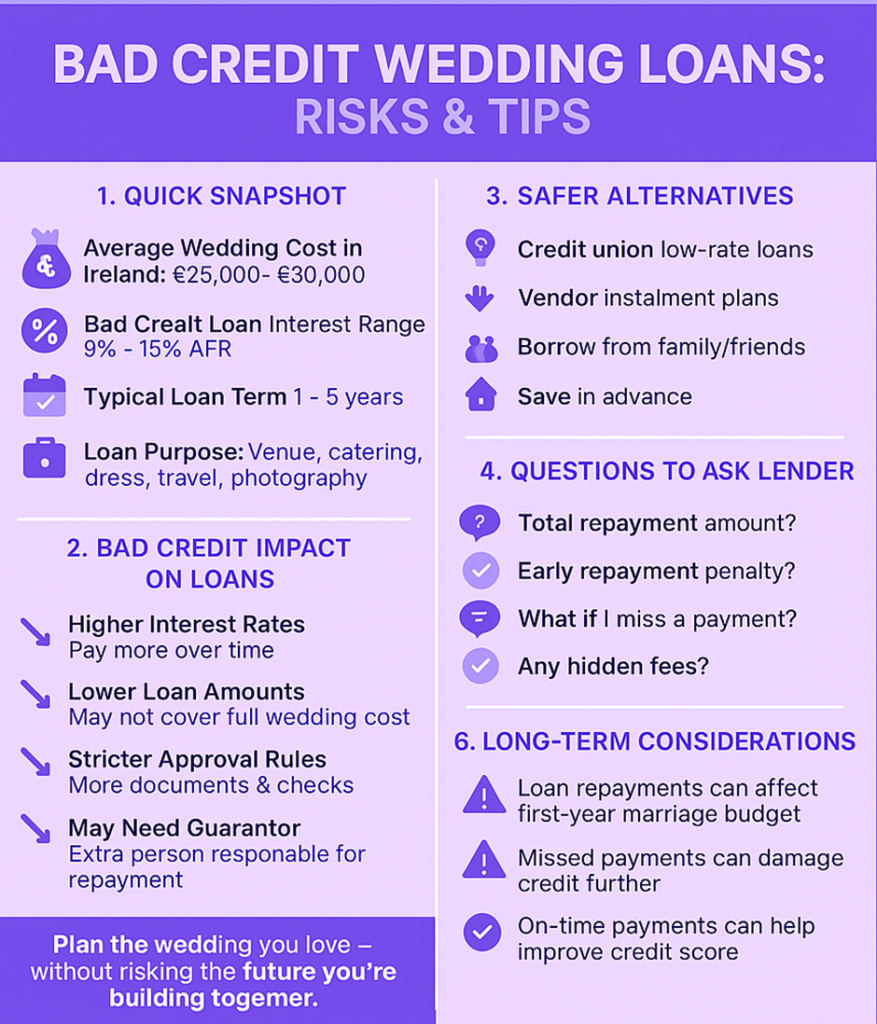

The average wedding now costs over €31,000. Many couples find themselves struggling between rising venue fees and growing guest lists. The lenders view credit scores below 580 as high risk for any loan. This often leads to rejections during a stressful planning period.

This guide explores which lenders work with bad credit histories. You’ll learn the costs hidden behind tempting offers from wedding loan companies. You can also know how you can get loans for bad credit with instant approval. Our advice helps you decide if borrowing is the best for your specific situation.

What Is a Wedding Loan?

A wedding loan helps couples fund their special day without emptying savings accounts. These personal loans provide quick access to cash specifically for tying the knot. Most lenders offer between €5,000 and €25,000 with terms ranging from one to seven years.

You can pay for everything from the venue deposit to those stunning floral arrangements. Many couples use the funds for unexpected costs that arise during the planning process. You can also get personal loans in Ireland online easily. This makes the process more appealing for the couples.

The wedding loans provide a fixed monthly payment you can budget around. Application processes are typically quick, with some online lenders giving answers within hours. Here are some more perks of these loans:

- No collateral is usually required

- Funds typically arrive within days

- A fixed repayment schedule helps with budgeting

- Some lenders offer payment holidays

- Early repayment options may be available

Pros and Cons of Taking Out a Bad Credit Wedding Loan

Here is the table on the pros and cons of taking out wedding loans with bad credit:

| Pros | Cons |

| Allows you to have your dream day without years of saving | Much higher interest rates than those with good credit |

| Funding arrives quickly, often within days of approval | Monthly payments might strain your new marriage budget |

| A fixed payment schedule helps with planning household costs | Could further damage your credit if payments are missed |

| Credit unions may offer better terms than traditional banks | Many lenders charge application fees regardless of approval |

| Some lenders specialise in bad credit situations | The total cost of the wedding increases significantly with interest |

| Can consolidate various wedding costs into one payment | May require security or collateral to offset the risk |

| Successfully repaying improves your credit score over time | Limited borrowing amounts compared to good-credit applicants |

| Provides a backup for unexpected wedding expenses | Starting married life with additional debt |

Average Wedding Loan Rates in Ireland

Wedding loan interest rates in Ireland differ according to your credit score. Consumers with high credit scores can get rates of around 6-8%, but consumers with poor credit scores usually get higher charges between 15% and 24%.

The bride and groom can borrow between €12,000 and €15,000 for their wedding. At 10% interest paid over three years, monthly instalments would be approximately €387 for a €12,000 amount. The same amount is spread over five years; the instalment will be €254, but it raises the amount of interest paid.

Most lenders will charge setup fees between €60 and €150, which become part of your loan. Some couples choose shorter terms at a higher monthly payment to minimise total interest. Almost all wedding loans have fixed interest, and the lenders determine amounts based on your income, not your wedding budget.

Questions to Ask Before Signing

The couple should protect themselves by asking some questions before taking a wedding loan. Many lenders must legally provide loan details, but some facts are in the small print.

You should be getting the clear answers now to save you from surprises later. The loan agreement might seem dull, but it controls your money for years to come. Here are some questions to ask before signing your name.

- What’s the real cost after adding all fees and interest?

- How much will my credit score drop if I miss one payment?

- Can I pay extra when I have spare cash without penalties?

- Are there charges for setting up direct debits or paper statements?

- Will my rate increase if the national interest rates go up?

- What happens if I need to change my payment date occasionally?

- Is payment protection insurance included or pushed as an add-on?

- How quickly can I access my loan once approved?

- Can I get a discount for setting up automatic payments?

- Will paying off early save me money or trigger penalty fees?

Conclusion

Your wedding marks the start of a financial journey together. You should consider all funding options. Bad credit doesn’t mean giving up on your wedding dreams completely.

Many venues now offer smaller, intimate packages with significant savings. You make sure it aligns with your long-term goals as partners.

Wedding Loan FAQs

What is a wedding loan?

A wedding loan is a personal loan used to cover ceremony costs. The money is credited as a lump sum, which you pay back in fixed monthly amounts.

Who can apply for a wedding loan?

The residents aged 18+ with a steady income can apply regardless of relationship status. Most lenders want to see an employed status for at least six months.

How much can I borrow?

You can ask about your exact amount to the lender, who will decide it based on your income and existing debts.

Can I repay the loan early without penalties?

Many lenders allow early repayments without any penalty. You can search for the right lender to get these benefits.

What documents do I need to apply for?

You’ll need recent payslips, three months of bank statements, and a valid ID. The self-employed applicants must provide two years of tax returns.

Will the loan affect my credit rating?

Every loan application causes a temporary drop in your credit score. Your on-time payments will gradually improve your rating over time.

How quickly can I get approved?

The online lenders are pretty quick and often approve applications within hours. You can get the loan amount in just 1-3 days. The banks might take 5-7 working days to process everything.

What happens if I miss repayments?

You might have to pay late fees of around €20-€35 per missing payment date. Your credit score will drop, and the lender may contact you directly. The debt collectors might get involved after multiple missed payments. You can ask the lenders if they can offer payment holidays before missing a due date.

James Wince is the lead author and financial expert at MyLoansBoat. With a decade-long journey in the financial market, he has actually amassed comprehensive understanding and hands-on experience, which he gives his informative, useful, and reader-friendly posts. Covering a broad spectrum of financial subjects – from personal loans to business financing, mortgage refinancing to debt consolidation- James has an incredible capability to break down complicated financial lingo into understandable language, permitting readers to make knowledgeable choices. Enthusiastic about financial literacy, James’s objective is to browse our readers through the frequently frustrating seas of finance.