Are you struggling with bad credit in Ireland? The borrowing market has been transformed, and most lenders do not hesitate to deal with individuals who have credit issues. The Central Credit Register score is important, but not the last word on granting money.

This manual takes you through the process of locating loans at rates. We have made the difficult task of researching what lenders will say yes when others say no. You will know ways to get low-interest bad credit loans in Ireland.

You will find out what kinds of loans are right with you, how quickly the process actually is, and easy tips on how to negotiate better deals. You have to understand where to look and how to portray yourself as more than a credit rating.

How Bad Credit Affects Loan Options?

Your credit score follows you everywhere, affecting what money options you can access. The banks often slam doors shut when they see poor credit history in your file. They worry you won’t pay them back, so they either reject you outright or make borrowing much harder.

They protect themselves by charging higher interest rates when lenders do approve you.

This risk premium means you pay far more than someone with good credit for the exact same loan. Most bad credit borrowers end up with small loan amounts. This is just enough to solve your immediate problem, not your long-term needs.

The repayment terms shrink as well. Instead of comfortable 5-7 year terms, you might get just 1-3 years to pay everything back.

Paperwork becomes another headache. You can expect to provide tons of documents proving your income, spending habits, and bill payment history. Some lenders might even call your employer directly to verify your job.

- Bad credit loans often come with strict spending rules

- Weekly payments might replace monthly ones for closer monitoring

- Credit unions may request in-person interviews before approval

- Some online lenders use alternative scoring methods beyond traditional credit checks

- Rejection can further damage your score through repeated hard searches

| Documents Needed for Loan Application | ||

| Document | Purpose | Format Accepted |

| Photo ID (Passport/Driving Licence) | Identity check | Scan/Photo |

| Proof of Address (Utility Bill) | Address check | Dated within 3 months |

| PPS Number | Tax/identity link | Card or letter |

| Payslips (3 months) | Income proof | PDF/Scan |

| Bank Statements (3-6 months) | Spending review | PDF download |

| Employment Letter | Job confirmation | Signed by the employer |

| Proof of Benefits (if applicable) | Income proof | DSP letter |

Types of Low-Interest Bad Credit Loans in Ireland

The affordable loans with bad credit aren’t impossible in Ireland. Several options exist that balance reasonable rates with your credit situation.

Credit Union Loans

Credit unions offer some of the best deals for people with credit troubles. Unlike profit-hungry banks, these member-owned groups care more about your personal story than just numbers. Their rates stay capped at 12.68% by law, much lower than many alternatives.

You’ll need to join first and start saving, even just €5-€50, before applying.

Your neighbourhood credit union knows the community and shows more flexibility with lending decisions. The loan amounts range widely from small €500 emergency loans to substantial €50,000 borrowing for bigger needs.

Online Personal Loans

The online lenders offer streamlined applications you can complete in minutes. This is why it is easy to get loans from an online private money lender. Their APRs vary widely from decent 9% rates to eye-watering 49% depending on your credit profile.

Most perform soft credit checks first, so you can check eligibility without hurting your score further. Once approved, everything happens electronically, such as e-signatures, account verification, and money transfers within 1-3 days. These loans typically range from €1,000 to €25,000.

Guarantor Loans

A trusted friend or family member as a guarantor can help a lot. This second person promises to pay if you can’t, reducing the lender’s risk substantially. Your guarantor needs good credit themselves, as they’re essentially lending their creditworthiness to you.

These loans often approve amounts up to €15,000, ideal for debt consolidation or major purchases. The rates typically fall somewhere between prime loans and high-interest bad credit options. This also offers a middle ground that might save you thousands over the loan term.

What to Expect with Fast Approval Loans?

The application itself usually takes just 10-15 minutes online. The lender only asks for basic personal and financial details. Most lenders promise decisions within 1-24 hours, depending on their verification process.

Getting the money takes slightly longer, typically 1-3 business days after approval. Some newer fintech lenders offer same-day transfers for urgent situations. The document requirements remain fairly standard across most lenders.

You’ll need your ID, proof of address, and income documents ready to upload. Your PPS number is essential for verification purposes. Most lenders also want to see 3-6 months of bank statements to check your money habits.

- Approval doesn’t always mean instant access to funds

- Some lenders conduct phone verification calls before releasing money

- Weekend applications are typically processed on the next business day

- Pre-approval offers may still change after full document review

- Direct deposit to your current account speeds up the process compared to checks

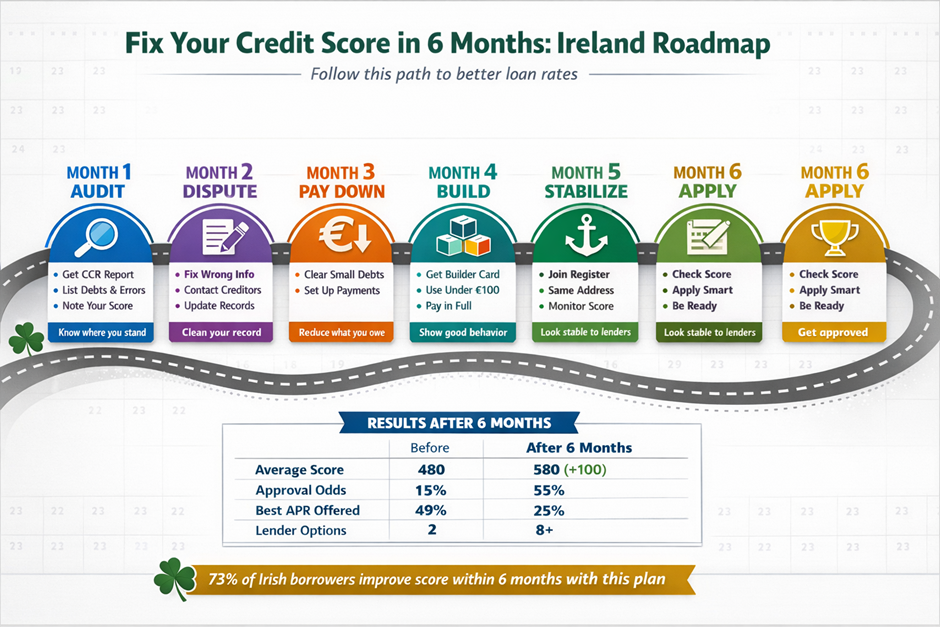

How to Get Lower Interest Rates with Bad Credit?

Step 1: Improve Your Application

You can start by cleaning up your finances before applying. You can pay down existing debts as much as possible to improve your debt-to-income ratio. This shows lenders you’re not stretched too thin already. You can check your Central Credit Register report for mistakes and get them fixed.

You gather strong proof of steady income through recent payslips or tax returns. A guarantor improves your rates if someone trusts you enough to co-sign. You can also put up security, like a car or savings account, to lower interest.

Step 2: Compare Lenders Properly

You can always compare using APR figures, not monthly rates that hide the true cost. Knowing the total repayment amount is a good way of understanding the exact amount of money that you will pay over the term of the loan. Checking for hidden fees is also an option, and you can especially look for lenders who do not have an early repayment penalty.

You avoid any broker charging upfront fees. The legitimate lenders take their cut from the loan itself, not your pocket directly. You can read recent reviews on Trustpilot and Google. The Competition and Consumer Protection Commission provides free comparison tools that are very helpful for consumers.

Step 3: Build Credit Before Applying

You take a few months to boost your credit score before applying if time allows. You can pay every single bill on time for at least 6 months straight. You can get on the electoral register at your current address, as this confirms your identity to lenders.

You can consider getting a small credit card, using it for minor expenses, and paying it off completely each month. Limit new credit applications to avoid multiple hard searches. Keep old accounts open even if unused, as account age helps your score. Show you can handle various commitments.

Conclusion

Your application creates a trace in your credit file, and therefore, you need to make an informed decision before you apply. It is possible to begin with credit unions, in case you have time to establish membership, or consider the possibility of finding a guarantor, in case a person trusts you to be able to repay the loan.

Online lenders are convenient, and they balance their overall costs fairly. You never sign something without reading its fine print. However, and most importantly, take any new loan as an opportunity to re-establish your credit.

James Wince is the lead author and financial expert at MyLoansBoat. With a decade-long journey in the financial market, he has actually amassed comprehensive understanding and hands-on experience, which he gives his informative, useful, and reader-friendly posts. Covering a broad spectrum of financial subjects – from personal loans to business financing, mortgage refinancing to debt consolidation- James has an incredible capability to break down complicated financial lingo into understandable language, permitting readers to make knowledgeable choices. Enthusiastic about financial literacy, James’s objective is to browse our readers through the frequently frustrating seas of finance.